Herman er utdannet siviløkonom fra BI med etterutdannelse gjennom graduate programmet til A.P Møller-Maersk. Med mange års erfaring fra finans og shipping tok han i 2015 med seg sin erfaring fra disse markedene inn i Malling & Cos satsing på analyse av næringseiendom, hvor han har ansvaret for investeringsmarkedet. Herman brenner for å bruke analyser av investeringsmarkedet til å se attraktive muligheter og det beste beslutningsgrunnlaget for både kunder og eiendomshusets egne rådgivere.

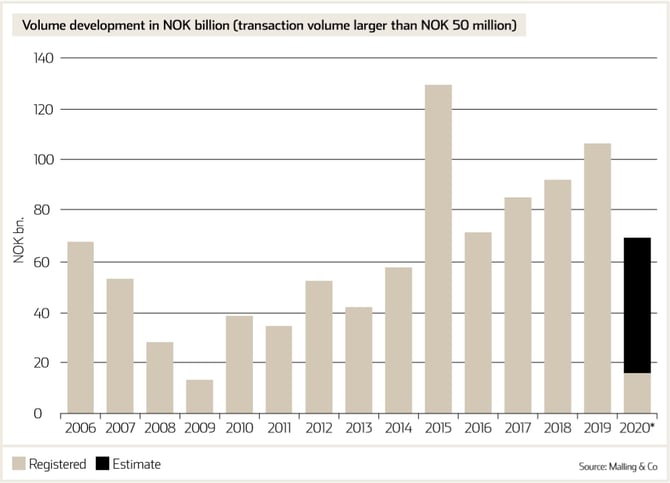

So far this year, we have registered a total transaction volume of NOK 17.8 billion, split between 67 transactions. With the Covid-19 outbreak, a very promising start to the investment market activity in 2020 came to a halt. But both from our survey and contact with investors, there is still high interest in commercial real estate as interest rates are coming down to record low levels. While most structured processes have been put on hold, there is still a steady flow of transactions done off-market. And to answer the big questions on everyone’s lips, prices have not moved significantly. While some uncertainty can be attributed to future rental prices, we have not seen any sign of anything but very modest discounts between 0 % and 5 % on pre-corona levels. Yet, with the underlying risk of the economy in general, and how the pandemic evolves going forward, we predict through our main scenario that Norwegian CRE will be firing back up in the second half of the year for a full year estimate of NOK 70 billion for 2020, a decrease of roughly 35 billion from 2019.

Banks are still there for their clients

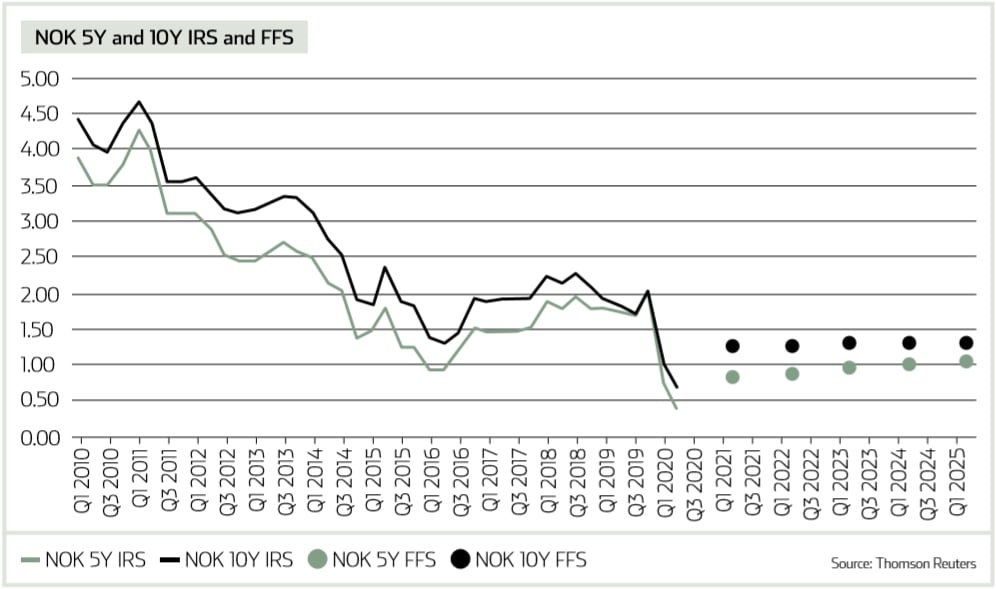

After the shock effect of society basically being shut down and interest rates going through the roof, central banks came to the aid of financial markets and we have since seen record low interest levels. And the low levels are expected to last for years to come, as the forward starting swaps as far out as 5 and 10 years are more or less flat too. After a brief halt while everyone was finding their footing, banks stepped up for their customers. Solid projects are still welcomed and supported. Although margins have been adjusted upwards, there is in sum still a lower total financing cost for many, as underlying interest rates have plummeted.

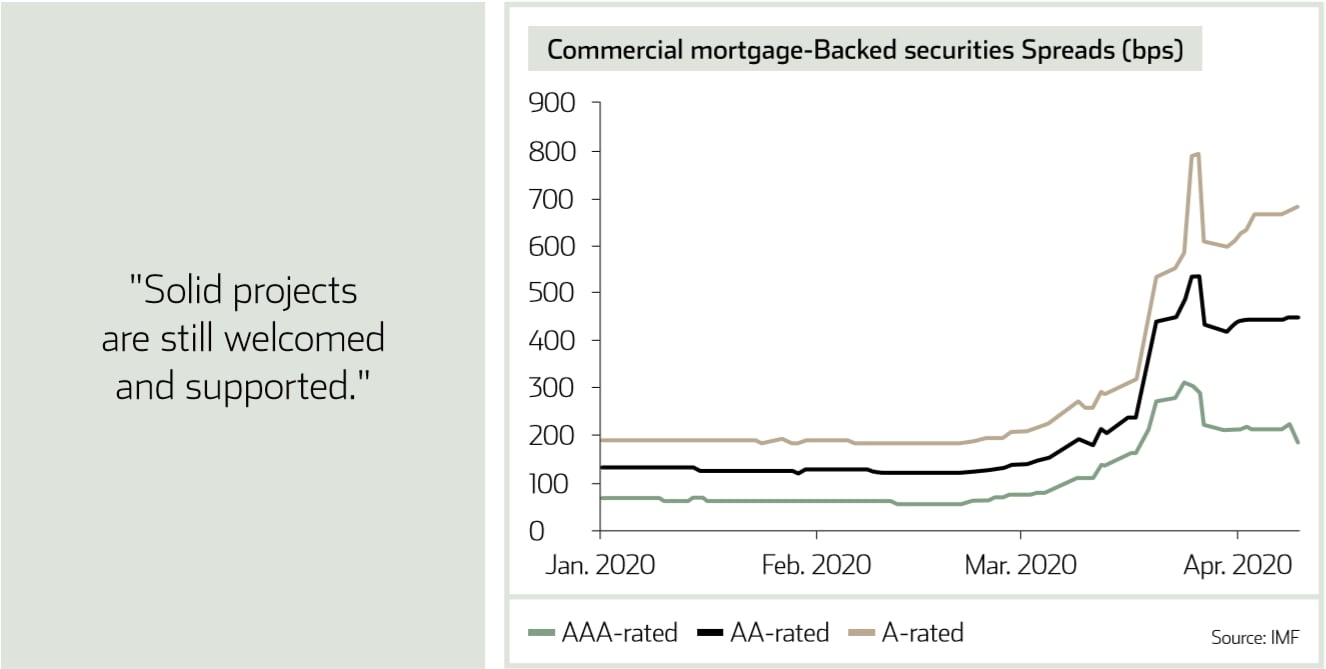

Bond financing is a different story now. Margins have increased substantially and are in most cases not competitive with bank financing. The big increase can be seen in our graph of CMBS spreads. And although they have come back down a little, the spreads factor is still 2-3 times higher than pre-Covid-19. Also worth noting is how prime AAA rating has come further back down of late, while AA-rating remains flat, and A rating is on an increasing trend again. Investors demand a premium for risk, and a flight to safety seems prevalent.

A safe harbour in turbulent times

Our regional overview for 2020 reveals that Oslo is a safe harbour in stormy weather, not only literally but also figuratively. Almost 60 % of the volume is from the Greater Oslo region. And though, admittedly, much of this volume is from pre Covid-19 lockdown, we are seeing more activity taking place in this region than that being reported from other major regions. Our main scenario is, however, still a gradual increase in activity across all regions towards summer, and a close to fully operational and functioning investment market over the summer. The second half should see the difference in volume share somewhat equalised towards a more normal share for the other regions outside of Greater Oslo. This is also supported by the Prime office yield levels across the regions, which have remained stable or decreased since our last report, and with our expectations that a shift is skewed towards a yield compression.

This is a section from our latest Market Report. Read more in-depth research and analysis into property market trends, forecasts from our specialist research teams here;